Table of Contents

Chapter 13 Bankruptcy – the Ultimate Guide

What is Chapter 13 bankruptcy? Chapter 13 bankruptcy is like debt consolidation, but better. It’s a solution for people who have some money to pay some of their debts back. In five years from now, paying minimums on all your debt, you’d still owe much of your debt. It’s because of that darned interest, and you’re barely paying principle. Chapter 13 bankruptcy fixes the interest problem.

Who am I? I’m a Los Angeles bankruptcy lawyer. For years, I have served as the Chair of the Chapter 13 Committee of the cdcbaa. I’ve successfully confirmed hundreds of cases for my clients, and led those cases to discharge. I’ve been on committees with judges, trustees, creditor lawyers, and other debtor attorneys that have worked on forms and rules changes for our entire district, and have hosted, moderated, or presented on panels on the topic of Chapter 13 bankruptcy to other lawyers. Here I share just some of what I’ve learned over the last twenty years to help people trying to learn about this mysterious area.

What is a Chapter 13 bankruptcy?

Filing bankruptcy under Chapter 13 is for people who have some discretionary income. With this extra money each month, the consumer bankruptcy debtor can repay some or all of their debts.

Discretionary income is money left after their normal and usual monthly expense are deducted from monthly income. For this reason, a Chapter 13 is called a “Wage Earner Bankruptcy” The focus is having money to repay debts, which we call “budget surplus.”

60 Monthly Payments

A big difference between Chapter 7 bankruptcy and bankruptcy chapter 13 is that there are monthly payment plans for the chapter 13 debtor. The Chapter 13 plan payments can even help you pay back tax debt, which in Chapter 7 is usually not discharged. Plan payments are made to the Chapter 13 Trustee over a period of (usually) 5 years.

What are these payments? These payments are usually to firstly, tax debt. Secondly, they go to whatever you may be behind on your mortgage payment, or sometimes your car loans. Finally, they’ll go to pay some or all of your credit card debt. Chapter 13 bankruptcy therefore is a good way to stop foreclosure and save your house, as well as stop creditor harassment. And of course, all the California bankruptcy exemptions still apply, so you can keep your stuff.

Chapter 13 was intended to give the person with income a chance to make affordable installment payments. This comes out of future income so that creditors get paid at least something. The good new for you is that there is no liquidation in Chapter 13. The Chapter 13 bankruptcy trustee doesn’t take things. Generally, you keep your stuff.

You’re going to want a skilled Los Angeles bankruptcy attorney to help you so you can make your payment plan no more than you can afford for your Chapter 13.

The Stuffy Definition: Wage Earner Bankruptcy

Chapter 13 of the Bankruptcy Code lets debtors under Court protection apply a portion of future earnings to the repaying some or all their debts over time. Creditors can’t do anything during this time to collect the debts. The automatic stay protects the debtor while a plan of repayment is carried out. It is similar to a Chapter 11 Business Reorganization. In fact, Chapter 13 is sometimes called “Consumer Debt Adjustment.”

Consumer Chapter 13 Bankruptcy Overview

You currently have enough extra money at the end of the month to pay your credit card minimum payments. This, of course, is getting you nowhere. You’ll have the same debt in 8 years, and will still be paying $700 or $1000 or whatever it is each month… forever. There’s a way to eliminate debts on your terms, like debt consolidation.

Or you’re behind in your mortgage payments, and want to keep your home. And you have extra money each month you’d like to use to catch up, but the mortgage company won’t work with you. This is one advantage of Chapter 13 over other types of bankruptcies.

In either situation, you can take that money you have left at the end of the month and start reducing the debt you owe so that you’re out of debt in 60 months.

Chapter 13 Bankruptcy Process

The process for filing Chapter 13 is a maze-like process, and you will want to have an attorney by your side. The paperwork involved is truly overwhelming, and the time is much greater than a Chapter 7 bankruptcy.

Preparing the Petition and Plan

Bankruptcy Petition

Like any bankruptcy case, you will need to have a bankruptcy petition for the court. This is often 30-50 pages thick and lists your debts, possessions and other information in a very particular order and fashion.

Payment Plan

The payment plan is the key to a Chapter 13 bankruptcy, and what sets it apart from a Chapter 7 bankruptcy. It sets out all the ways which the debt will be handled during the administration of the bankruptcy by the Chapter 13 Trustee. How much unsecured debt will be paid? Are you going to keep paying on the car, or give it back for a voluntary repossession? What about the mortgage: will it be caught up if you’re behind to avoid foreclosure, or if so, how long will it take to pay the arrearages that you’re behind?

In short, a lot of precise and important calculations go into the bankruptcy plan payment with the aim of determining the number that matters most to the debtor. This number, of course, is the monthly payment. You’ll pay this monthly payment for 60 months (yes, that’s 5 years). By definition, you’ll be able to afford it. A good bankruptcy attorney can ensure you are able to make the payment, but that it’s also something that can be accepted by the bankruptcy trustee and creditors.

Court Involvement

Filing the Bankruptcy Papers

After these are ready, the bankruptcy petition and payment plan are submitted to the U.S. Bankruptcy Court. The papers are filed and the case gets a number and the ball is rolling.

The Meeting of Creditors (341A)

Like a Chapter 7 bankruptcy, you must go under oath with penalty of perjury regarding the facts that are contained in your bankruptcy petition. You will need to appear in bankruptcy court to answer some brief questions. This is the 341(a) Meeting of Creditors.

Confirmation

After the bankruptcy court date, your attorney will need to return to court. This involves making sure that the numbers all add up, your chapter 13 payment plan is fair to both you and your creditors, and of course, to accept your next monthly payment. If all goes right, your plan will be “confirmed,” your plan is accepted and everything is on automatic pilot.

After Bankruptcy Court

After confirmation, from this point forward, you will just mail your monthly payments to the chapter 13 trustee. There usually are a couple of restrictions, such as notifying the trustee if you get a change in your income. Further, you’re not to get more than $500 on any future debt without permission. Something to remember: any extra money above and beyond your normal monthly expenses goes to the bankruptcy for debt. Consequently, the bankruptcy court and trustee follow anything that changes the formula of your confirmed plan. This is why the Chapter 13 trustee needs to see your tax returns, and usually gets any tax refund.

Calculating the Bankruptcy Plan Payment

Chapter 13 Plan Payment, Generally

The Chapter 13 bankruptcy plan payment is often whatever you can afford. That is, it’s what’s left after your projected monthly income and reasonable and necessary expenses. By definition, the bankruptcy plan payment is affordable, and typically less than paying all your credit cards directly.

However, that’s not always the case. There are other factors that can set the “floor” of your Chapter 13 plan payment amount. Of course, if you can afford more than your floor, you normally pay what you can, up to the full amount of your unsecured debt , which I’ll call the “ceiling.” Somewhere between the floor and ceiling is your Chapter 13 plan payment amount.

Factors that can affect the bankruptcy plan payment

There are lots of things that can raise the “floor” and impact what your Chapter 13 bankruptcy plan payment. These exact figures aren’t usually known without some research or work.

- the result of the long B22 form which analyzes all your pay stubs and income the past six months

- while no one takes your assets in Chapter 13, they factor in what you would’ve lost in Chapter 7

- the amount of your priority tax debt (both state and federal taxes)

- the value of your financed car which is old enough that you can cram down and pay only what it’s worth, not the loan amount

- the amount of mortgage arrearages, including all late fees

- current value of any judgment liens on your residence

- balances of all your credit cards bills, including nonpriority IRS and FTB debt

- how much you owe in unpaid property tax debt

- and more

Can you say with any certainty the values of any of these variables, let alone all of them? Of course not. Heck, even the answer to the first bullet point about the B22 often isn’t known until I see all your paystubs and bank statements. The bottom line is that while the ceiling is fixed to “all,” the floor of what you pay for your bankruptcy plan payment can rise or fall based upon the responses to all these and other factors.

So what’s my Chapter 13 plan payment amount?

Few of these factors are known for sure at the bankruptcy consultation. Consequently, anyone at the first meeting who predicts with any confidence your projected Chapter 13 plan payment amount is potentially ignorant, misleading, or both. The one exception is when someone says you need to pay all your debt, what we call a 100% plan, but even then, we’re not always sure of the exact balances of all your debts. Having a 100% plan can make it more sensible to sell a home in Chapter 13, give you less stress and more disposable income, and help you keep your tax refunds in Chapter 13.

However, in my best effort to help you, I can say this: while the above factors can throw a wrench into the works, your Chapter 13 bankruptcy plan payment is often based upon whatever you can afford, using average income minus reasonable and necessary living expenses.

Can I later reduce or change my Chapter 13 payment

Usually, yes, you can petition the court to reduce your plan payment in Chapter 13 if there’s a change of circumstances. This is done by a Motion to Modify, and needs to get approval from the trustee and, of course, your bankruptcy judge.

Why do I need a Chapter 13 bankruptcy lawyer

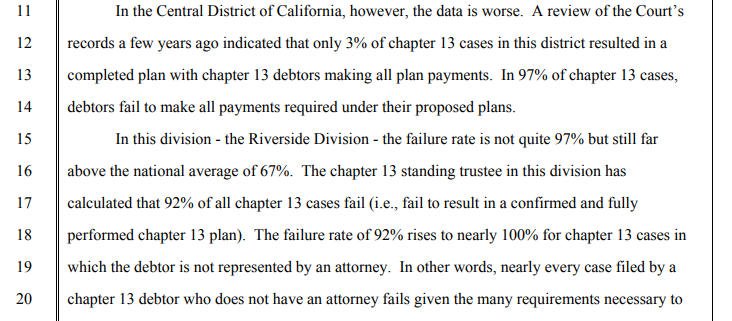

Chapter 13 bankruptcy cases are ones in which it is hard to be successful. Judge Johnson of the Central District of California (where Los Angeles is situated) has researched the topic. In his standing order, Judge Johnson finds that nationally, only 33% of Chapter 13 cases succeed. Locally, however, it’s much more rare. The judge finds that in the Central District of CA, only 3% of Chapter 13 bankruptcy cases succeed. He also found that this number drops to 0% when there’s not a bankruptcy attorney helping the debtor.

CDCA Low Chapter 13 Success Rates

Quoting the bankruptcy judge:

“A review of the Court’s records a few years ago indicated that only 3% of Chapter 13 cases in this district resulted in a completed plan with Chapter 13 debtors making all plan payments.”

That’s not a typo: 3%.

There’s no doubt that Chapter 13 bankruptcy is difficult to learn and navigate for the Los Angeles bankruptcy filer. Anyone who wanted to do one would need a bankruptcy lawyer to even out the odds of success. You’d want a bankruptcy attorney who had experience with Chapter 13. Not just experience, but success with these challenges.

Los Angeles bankruptcy attorney Hale Antico has Chapter 13 success

Bankruptcy filing statistics show that from 2008 to 2011 there was a peak of Chapter 13 filings.

Between 1/1/2008 and 12/31/2011, Los Angeles bankruptcy attorney Hale Antico filed 177 Chapter 13 cases.

Successful cases take 5 years to earn a discharge; unsuccessful cases end sooner.

Between 12/31/2013 and 12/31/2017, there were 104 of these earlier Chapter 13 bankruptcy cases which received discharges.

104 divided by 177 is 59%.

Or viewed differently:

Chapter 13 Bankruptcy Success Rates

The stats say you need an attorney for Chapter 13 bankruptcy. But not just any 3% successful bankruptcy lawyer. It would be a good move to go with one of the best bankruptcy attorneys whose success rate is almost double the national average, and 20 times higher than the local success rate.

Summing up Chapter 13 Bankruptcy

All in all, Chapter 13 bankruptcy is a successful debt consolidation where you pay a fixed payment for a fixed term. Everything after the term that didn’t get paid is discharged. Filing it freezes interest. Creditors can’t sue you. You just pay back what you can. This is often cheaper than what you’re currently paying all those minimum payments combined before the bankruptcy. Why? Because without bankruptcy all those minimums only go to interest. Chapter 13 bankruptcy works to get you out of debt.

Read my article of things to do (or avoid!) before you file bankruptcy. We’ve helped thousands of people in Los Angeles file bankruptcy. We’d be honored if you’d let us put our success to work to help you, too.