Table of Contents

Tax Refunds & Returns in Chapter 13

Can I keep my tax refund in Chapter 13? It depends.

You ask, “can I keep my tax refund in Chapter 13?” Maybe. Chapter 13 tax refunds can be the one thing that sinks a successful bankruptcy case if you keep them. Things are sailing along, and suddenly, things go sideways. Fortunately, there are solutions and ways to fix it and save your case, and ultimately, the discharge you’re working towards.

I’m a Los Angeles bankruptcy attorney, serving all of Los Angeles County and the Central District of California. For years, I have served as the Chair of the Chapter 13 Committee of the cdcbaa, the largest association of bankruptcy attorneys in Los Angeles representing debtors. I’ve successfully gotten hundreds of Chapter 13 bankruptcy cases confirmed, and led a very high percentage of them successfully to discharge. I’ll be writing specifically about practice in the Central District of California, using our forms, CDCA local rules, and other local practices. If you’re anywhere else, the following may not apply to you; seek a bankruptcy lawyer local to you. But if you’re in Los Angeles, Ventura, or Orange County, read on.

Chapter 13 Tax Refunds: the rule

The general rule in Chapter 13 bankruptcy is that you must turn over tax refunds over $500 each year to the Chapter 13 trustee, unless it’s a 100% plan. Commit this key point to memory: if there is a tax refund in your Chapter 13 bankruptcy, don’t spend it until you talk with your attorney. There is a very good chance that you will need to send it to the trustee.

You are also supposed to provide to the Chapter 13 trustee your tax returns each year, and often also your paystub (or more) and W2, for income-tracking purposes.

Whether or not the plan is what we call a “hundred-percent plan” can make all the difference here. It can make your life easy and not cramp your style. Alternatively, it can require that you turn over that sizeable tax refund check each year.

What is a 100% Plan in Chapter 13

Keeping it basic, a Chapter 13 100% plan is where all the general unsecured debt gets completely repaid. Usually, this means that the credit card debt gets paid, dollar for dollar over the Chapter 13 plan term. In the Central District of California, bankruptcy attorneys refer to this as Class 5 debt (or Class 5A), or more frequently, unsecured debt, or simply, the unsecureds.

In Chapter 13, you don’t always repay all your debt

Reviewing something I wrote about in my main Chapter 13 article, the plan payment in Chapter 13 bankruptcy is often what you can afford, after reasonable and necessary household expenses. Or put in other words, a lot of times (not always), you are paying what you can afford, and not all of the debt. Because the plan payment is usually driven by ability to repay and not debt size, this can result in you paying only a fraction of your debt.

Example: you can afford $400 a month for 60 months, but your unsecured debt (credit card) is $48,000. $400 x 60 is $24,000, divided by $48,000 is 1/2, or 50%. That’s grossly simplifying most cases, but that’s a 50-percent plan. The other 50% gets discharged at the end if you stick to the plan and make all your payments on time. You never have to pay the discharged half, they can never bother you again.

On the other hand, if you have enough cash flow each month where, in sixty months, you can pay all your credit card debts (because the monthly payment is bigger or the unsecured debt is smaller), that might become a 100% plan, and unlock all kinds of benefits and wonders.

Why do I have to turn over my tax refunds in Chapter 13?

You need to turn over your tax refunds in Chapter 13 bankruptcy because it’s closing a loophole. You over-withheld all year long, making your monthly payment small, then with the refund, get back all that withheld income at the end of the year. If you think about it in this extreme example, paying the trustee a dollar a month because that’s all you can afford, then you get $12,000 tax refund on April 15 isn’t fair. It’s a sweet deal for you, the debtor.

However, the trustee will argue (and be right) that you should have adjusted your W4 to lower and withhold the proper amount, increased your take home pay, and the plan payment would increase by approx $1,000 a month. To avoid the over-withholding backdoor loophole, you must send in your tax refunds if it’s not 100% plan.

The Central District of California uses a form plan. In it, there’s a paragraph that spells out to the debtor what is expected with tax returns, and what happens with tax refunds. This is part of every Chapter 13 bankruptcy filed in the greater Los Angeles area, and then the debtor signs it, and is mailed a copy along with the Notice of 341(a) Meeting when the case is filed.

What if my Chapter 13 bankruptcy is a 100% plan?

If it is a 100% plan, you’re already repaying all your general unsecured debt. You cannot pay more than all. So, when the refund comes, should you give it to your trustee? Ask your attorney. But generally, as long as you’re at 100%, the bankruptcy doesn’t need the refund.

Note: if you have a 100% plan and your bankruptcy gets modified during the bankruptcy term to pay less than a hundred percent to the unsecured creditors, you may need to pay to the trustee the past refunds you kept, retroactively.

As long as the Chapter 13 bankruptcy is paying all the debts, as a rule, the tax refunds don’t need to be turned over.

Does the Chapter 13 Trustee garnish my tax refunds?

No, the Chapter 13 trustee doesn’t normally intercept or garnish your tax refunds. You have to manually send the funds to her, at her normal payment address.

I have to mail in the entire tax refund, or I keep $500?

It depends. Look at the Order Confirming your Chapter 13 Plan (or the last order on motions to modify it). Usually, in the Los Angeles area where the Central District is, you get to keep $500 of each year’s refunds, but have to turn over the rest.

Does a given year’s tax returns offset each other if I owe on one?

Usually, yes, you get to offset the same year’s return. An example of this would be: let’s say on the federal tax return you got a refund of $1500. On the state tax return of the same year, you owe $400. You’d subtract the $400 from the $1500 (and presumably pay the state), then subtract $500 if your Order Confirming allows you to keep that amount. The result? $1500-400-500 = $600 sent to the Chapter 13 trustee.

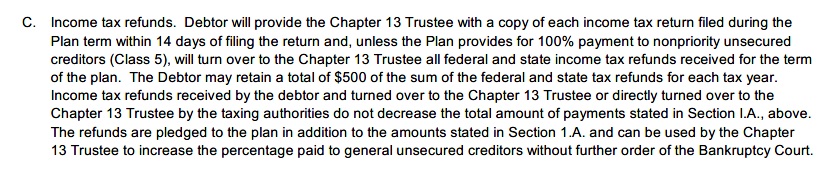

The Order Confirming is the Controlling Document in a Chapter 13

The judge’s order in your case is what matters. You have to do whatever the Order Confirming your Chapter 13 plan says you have to do. It is pretty specific on plan payment amounts, due dates, and the percentage that the general unsecured creditors are receiving. It usually is pretty clear about what happens with tax refunds. Read it closely.

Take a look at the above. It’s a paragraph from an actual Order Confirming Chapter 13 Plan from one of my clients. The Order Confirming says that it’s not a 100% plan, or the bottom checkbox would be checked. It says that all refunds go to the Chapter 13 trustee during the plan term. It says that you get to combine the state and federal tax returns. And it says the debtor gets to deduct $500. But again, read the specific language of the order which confirmed your case. Your mileage may vary.

Do I keep my tax refunds in Chapter 7 bankruptcy?

It depends. Chapter 7 is a different animal than Chapter 13 (see my article on different types of bankruptcies). As I wrote above, Chapter 13 is generally about paying back what you can afford, but you can’t usually make your take home pay artificially tiny and then pocket the refund. Chapter 7 is all about assets and stuff. The California bankruptcy exemptions allow for keeping a lot of things and money, up to a point. If you’re using the California homestead exemption, there’s a really good chance you won’t be able to protect your tax refund. See a bankruptcy attorney for specific advice about your unique situation.

I kind of skimmed above, what’s the rule on tax refunds again?

The general rule is this (say it with me): if you’re not paying back all your debt, you need to turn over your tax refunds to the trustee each year.

What about my tax returns then?

While we’ve been talking about tax refunds, you need to send the Chapter 13 trustee your tax returns each year also.

Why does the Chapter 13 trustee care about my tax returns?

When you send in your federal and state tax returns to the trustee each year, she’s reviewing a few things. First, she’s looking to see if you got a refund (see discussion above). Second, she’s looking to see your annual income, and comparing it to what you earned when you filed the case. Third, she may be looking for any windfalls you received the previous tax year.

If my tax returns show higher income, will my plan payment go up?

Not always, but maybe. See 11 USC 521(f)(3-4). Ask your bankruptcy attorney.

Oops, I forgot to submit my tax returns. The Chapter 13 trustee is filing a Motion to Dismiss.

Easy! Send the tax returns to her, usually accompanied with the other documents she’s requesting: a recent paystub if employed, a W2 for the most recent year, and a 1099, if applicable. Do this as quickly as possible and this should save your case. But beware, because…

Oh no! There’s a Motion to Dismiss because I failed to turn over my tax refunds

If your plan is less than 100% to the unsecured debt like credit cards, you need to send in your tax refunds each year to the Chapter 13 trustee. If for some reason you failed to do that, the bankruptcy trustee may file a Motion to Dismiss. This motion to the court and bankruptcy judge is seeking to end your bankruptcy, end the automatic stay protection, end your attorney’s representation, and leave you to fend off your creditors and debts outside the terminated bankruptcy case. It is very serious. But you have some courses of action:

Possible responses to a Motion to Dismiss for failure to turn over tax refunds

File a Motion to Modify Chapter 13 Plan

The first possible solution to Motion to Dismiss for failing to hand in your tax refunds is to file a Motion to Modify (also called MoMod). The Motion to Modify can ask the judge to retroactively suspend turning in your tax refunds for year(s) in question, despite the fact that you knew or should’ve known you were supposed to because you signed the Chapter 13 Plan and read the judge’s Order Confirming which required it.

This can be a difficult hurdle, and the facts and evidence matter. If the trustee is demanding $3,000 of tax refunds and you can point to a hospital bill where you were forced to pay $3,100 in cash that same tax year, that may be a reasonable expense which you can document with the evidence of the hospital bill and receipt that you paid it. Maybe the Chapter 13 trustee wouldn’t oppose your MOMOD and/or the judge would grant the Motion to Modify, and let you keep your tax refund.

Note that Motions to Modify are not guaranteed to work. There’s a lot of work that goes into MOMODs, and there will be legal fees approaching (or exceeding $1000) for the work to do a MOMOD. Weigh the pros and cons, including the likelihood of success. Consult with your bankruptcy attorney.

Respond to the Motion to Dismiss with a Payment Plan

As a rule, you should respond to the Motion to Dismiss the case with a response if you want to keep the case alive. If you don’t file a reply (technically, a response) to the trustee’s motion, it will be unopposed and the judge will likely grant it, ending the case, bankruptcy protection, and lawyer representation. If you are going to file a motion to modify, your response to the trustee’s motion should explain that. Here, though, you aren’t modifying, but requesting a chance to catch up and pay the tax refund in installments.

With the response, be very specific as to when the payments will be, and when the tax refund will be completely paid to the trustee. Ideally, you will turn over the tax refund before the hearing date. Being current by the hearing is your best chance at saving the case. Everything else is putting yourself at the mercy of the trustee, and the court.

Dismiss and re-file, getting a new 60 months

It’s definitely not ideal, but if the case gets dismissed, you can often re-file a new case. This will get you a new 60 months to repay debt, but also incur a new legal fee to prepare all the petition, schedules, compute and craft a new plan, and statement of financial affairs again.

Your best best is often to get current and turn over the tax refund to the trustee by the hearing, but again, ask your bankruptcy lawyer.

In short

A Chapter 13 bankruptcy case can have many twists and turns over the years between filing and discharge. One requirement is to turn over tax returns, and tax refunds, each year. If you are paying back 100% of your debt, life can be a lot easier. On the other hand, if you’re paying less than 100% of your debt, make sure you send in your tax refunds each year. If you forget, there may still be a way to save it. Failing to send in tax refunds for multiple tax years is a much harder sell, since it’s harder to trace the income to a particular expense. But if you’re able to make up the amount in payments, with the approval of the trustee and judge, you just may be able to save your case.